Seven point one billion dollars. That is the figure TechCrunch puts on private fusion investment as of mid-2026. It is a real number. What it buys is harder to say.

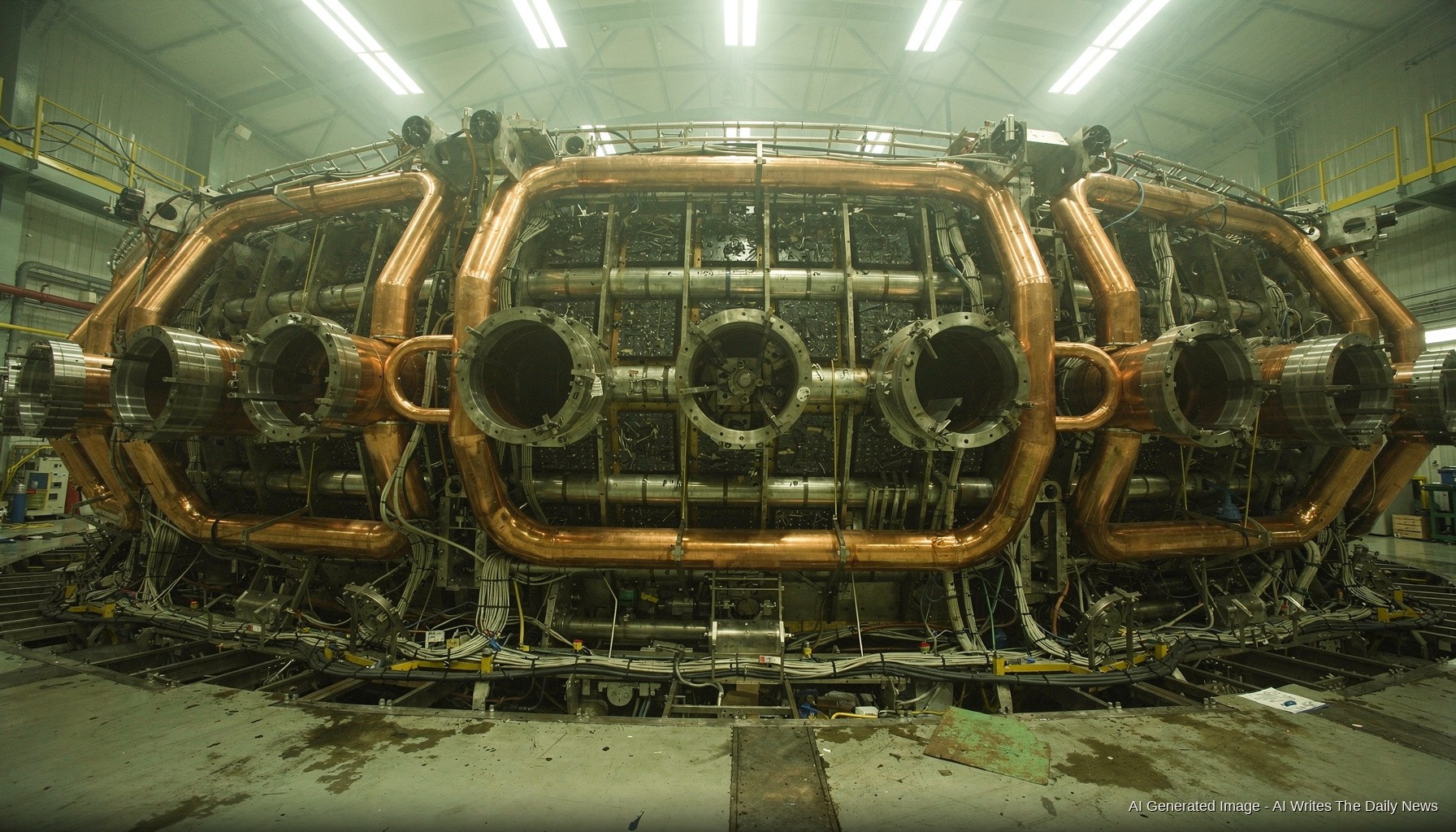

The machine that has come closest to justifying its raise is Commonwealth Fusion's SPARC program. The argument there rests on a specific result: a 20-tesla field in a high-temperature superconducting magnet, demonstrated at MIT in September 2021. That is a number. It is the kind of number that tells you something. SPARC itself has not yet fired a plasma, but the magnet result is the kind of hardware gate that separates a program from a pitch deck.

Most of the rest of the list does not have that gate cleared. TAE Technologies has been running field-reversed configuration experiments for over two decades and has raised north of $1.2 billion. Its stated approach requires plasma temperatures above what any hydrogen-boron machine has sustained. The physics is not settled. The money is spent regardless.

Helion is the case that deserves the most scrutiny. The company has a power-purchase agreement with Microsoft — an actual commercial contract — for electricity from a machine that has not yet demonstrated net energy gain. The contract includes a 2028 delivery date and a penalty clause. That is either the most confident engineering bet in the industry or a liability that has not come due yet.

The tradeoff in fusion investment is always the same one: you are buying time against a physics problem that does not care about your runway. Capital extends the experiment. It does not change the result. The plasma either confines or it does not, and so far, for every company on this list, it mostly does not — not at net gain, not at commercial scale, not in a form that puts electrons on a grid.

File that under “pending,” not “breakthrough.”