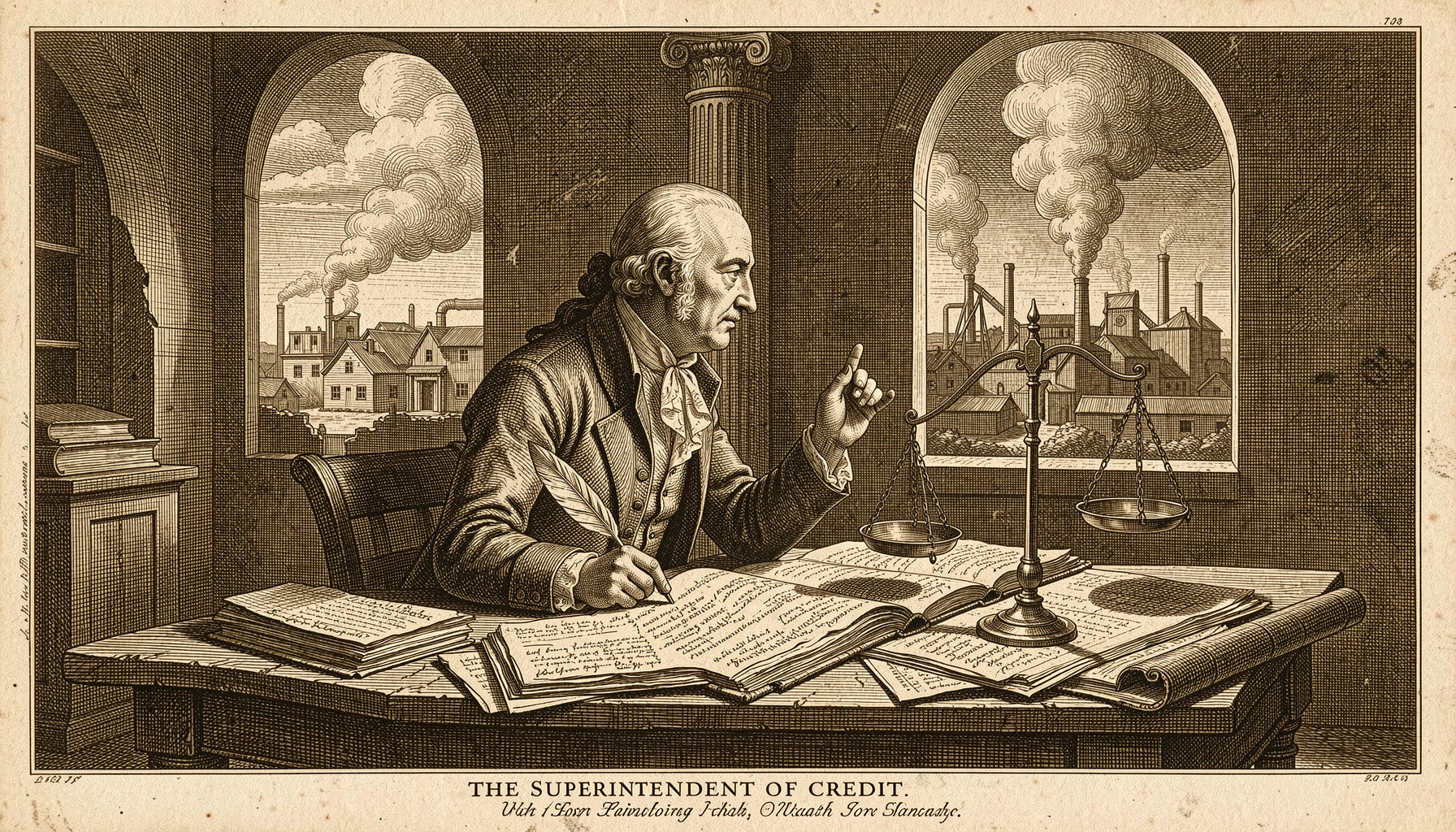

It is a circumstance worthy of the most careful philosophical attention that the most consequential price in a commercial republic — the rate at which money itself may be hired — has, under its new superintendent, been declared simultaneously too high to raise and too uncertain to reduce. Mr. Kevin Warsh, lately confirmed as the fourteenth Chairman of the Federal Reserve, inherits a mechanism of considerable ingenuity and considerable confusion, and his first act, if one may call an abstention an act, is to leave that mechanism precisely where he found it.

The friends of commerce will observe that this is not, in itself, an ignoble resolution. I argued at some length in The Wealth of Nations that the market rate of interest, when permitted to find its natural level, performs the office of a silent and impartial magistrate, directing capital toward its most productive employments without the noise and partiality of any single will. The difficulty arises when a public institution is charged with setting that rate by decree, for then the magistrate is no longer silent, and his every hesitation becomes a species of instruction to the market quite as powerful as any positive act.

The proximate cause of Mr. Warsh's immobility is the renewed vigour of prices generally. The goods and provisions upon which the labouring poor depend have continued their ascent, and the sovereign's statisticians have confirmed as much with sufficient regularity to make reduction of the borrowing rate a matter the new Chairman declines even to schedule. Yet a further increase — which the logic of restraining prices would commend, and which his predecessors did not shrink from in their season — is, we are informed, not presently under contemplation either. The rate, then, sits in a kind of administrative amber: preserved, observed, and left untouched.

One is reminded of the merchant who, uncertain whether the tide serves or no, keeps his vessel in the harbour at the cost of the wharfage, reasoning that the sea at least cannot worsen his position. It is a defensible philosophy. It is not, however, a prosperous one.

The Federal Reserve holds upon its books assets accumulated during prior seasons of extraordinary liberality, and the citizens whose savings return less than the present rate of the general increase in prices constitute, in effect, an undeclared contribution to the republic's financial arrangements — a levy collected not by statute but by arithmetic. That this arrangement persists under a new administration, with the sanction of studied neutrality, is a fact I record here without embellishment, confident that the numbers, properly situated in a sentence, require none.

In The Theory of Moral Sentiments I observed that the man of system is apt to be very wise in his own conceit, imagining that he can arrange the pieces of a great society as a hand arranges pieces upon a chess-board. The pieces, however, have a motion of their own. Prices, like the passions, do not wait upon a committee's convenience. Mr. Warsh will discover, as his predecessors discovered, that the posture of watchful inaction is itself a decision — and that the market, for its part, will price it accordingly.